In a Sense, Blockchains are Crappy Databases

source link: https://hackernoon.com/in-a-sense-blockchains-are-crappy-databases

Go to the source link to view the article. You can view the picture content, updated content and better typesetting reading experience. If the link is broken, please click the button below to view the snapshot at that time.

In a Sense, Blockchains are Crappy Databases

Audio Presented by

audio element.The fundamental purpose of cryptocurrencies is to exchange value with one another in a decentralized manner using state-free money, which is by definition censorship-resistant.

For a distributed network to be censorship-resistant, privacy is a necessity.

The earliest documentation of history has shown that the concept of money emerges organically within civilizations. A social lubricant for the exchange of goods is almost as important as the society in which it emerged. Aside from facilitating transactions, forms of money such as gold provided individuals the ability to store value. While money has been a natural by-product of the rise and development of any civilization, up until the 21st century, the concept of sound money has eluded us.

[Insert paragraph that takes a dump on fiat - centralized, money printer go brrr, double-digit inflation levels, artificially propped up asset prices, yadayada]

During the depths of monetary and fiscal despair, Satoshi handed us a working model of sound money on a silver platter, exactly when we needed it.

While Bitcoin gave birth to the revolution of decentralized platforms that serve as a means of transacting and/or storing value, the immutability and transparency features of the ledger have limited its applicability. When anyone can take a peek into the blockchain and scrutinize all transactional activity, privacy goes out the window. And with it, a host of use cases that require privacy as a feature.

The headline of this piece wasn't clickbait by any means. Public blockchains are, in a sense, dumb databases given the fact that the state and its changes are transparent.

Blockchains and Privacy

When you pay for your meal at a restaurant using a point-of-sale mechanism (debit card, credit card, etc.), would it make any sense to you if the merchant was able to access all of your payslips and banking activity as a result? One would naturally want that payment to reveal only the minimum necessary information required to facilitate the transaction.

Transparent databases are the societal equivalent of you leaving the front door of your house open for anyone to come and take a look inside. Cryptographic proofs are made use of in every block within public blockchains. But none of that cryptography is used to encrypt this transparent public data.

Privacy is imperative IRL. And perhaps even more so on the internet, given the fact that our lives and their various elements are increasingly moving to the virtual world. Privacy, as opposed to secrecy, is important not because one has something to hide. I believe it's important to make this crucial distinction between privacy and secrecy.

As written by Eric Hughes inA Cypherpunk's Manifesto:

"A private matter is something one doesn't want the whole world to know, but a secret matter is something one doesn't want anybody to know."

Think of it this way, when you hop in the shower to take a bath, you pull the shower curtains even though there's no one else in the bathroom with you. You do that for a sense of privacy. Not because you have something to hide.

Attempts at establishing secrecy arise when one has something to hide.

By no means do I advocate for secrecy. But I am strongly of the opinion that privacy - IRL and virtually - is a fundamental inalienable right of all individuals.

Privacy is not binary. It exists along a spectrum. The degree of privacy required by an average user of crypto transacting trivial amounts might be significantly less than what an institution consistently trading large volumes would desire.

Up until now, the need for privacy has somewhat eluded users and builders of crypto as there were greater issues at hand (security, scalability, decentralization, legislative uncertainty, the list is long). Some of these still persist. In spite of this, there have been a handful of advocates of privacy on blockchains. And I expect this trend and privacy-centric applications to burgeon over the next 1–3 years.

The needs of the average user have been limited to being able to transfer funds from A to B in an economically feasible manner. As individuals mature, they come to the understanding that the pseudonymity offered by the current generation of chains is merely a brittle sense of privacy. And that there are blockchain analytics firms such as Nansen, Chainalysis, etc., that can label and track public addresses in an increasingly granular manner.

In the case of blockchains, there is a high negative correlation between the size of funds you hold and/or regularly move with the degree of pseudonymity you eventually possess. A transparent ledger has posed numerous other problems like MEV, such as front running and back running, trading strategies of large investors being made public, and individuals being doxed based on their blockchain activity. If you're a crypto hedge fund allocating significant amounts of capital in these markets, you're delirious if you think that the degree of pseudonymity shields you from being doxed by others.

Pseudonymity vs. Anonymity

In any given crypto transaction between two parties, there are 4 key data points that can be considered as sensitive - the sender's address, receiver's address, IP addresses, and the amount transacted.

The first iteration of blockchains, which I'll refer to here as 'Gen 1', served as a store of value whilst maintaining the pseudonymity of network participants. This latter property is derived from the use of public addresses to facilitate transactions. In a block explorer, one does not see that Alice sent Bob 10 BTC, but the public address of Alice having sent the public address of Bob 10 BTC.

The concept of being pseudonymous is inherently linked to the ethos of Bitcoin and its creator - Satoshi Nakamoto. A pseudonymous entity. Pseudonymity is important as it offers a certain degree of privacy. But not enough. If a cryptocurrency is to become global, decentralized money, the state and its changes cannot exist on a public ledger. Everyone would be doxed instantly and everyone would be aware of one another's asset holdings.

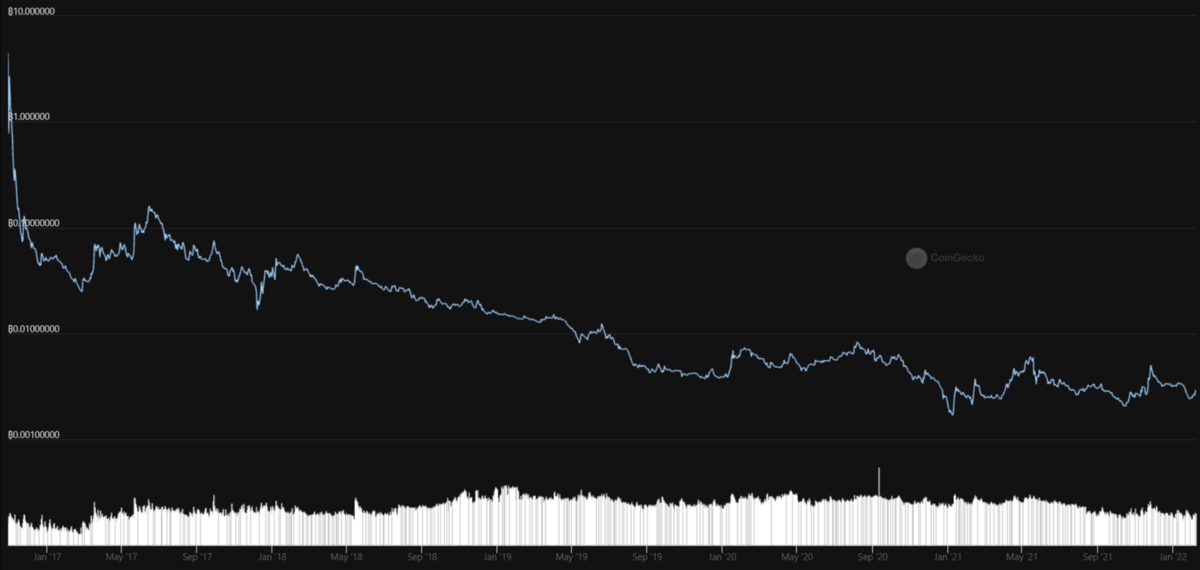

Zcach (ZEC) is a popular privacy coin that offers anonymity. A transaction made using ZEC does not publicly reveal transaction addresses and the amount transacted. In this manner, privacy coins enabled privacy as a product offering.

The problem with bitcoin or Zcash was that it virtually served no other purpose than being a store of value and facilitating the transfer of goods (to an extent). The need for a privacy-preserving store of value is debatable. Especially when BTC offers sufficient privacy guarantees to the average citizen (but certainly not to an activist in Hong Kong that’s targeted by the Chinese government for example). Hence one should not have to expose herself to the balance sheet risk that Zcash or Monero brings as opposed to bitcoin or ether.

Zcash (ZEC) to BTC chart from Jan ‘17 — Jan ‘22

Not to mention, the applications of privacy coins outside of their own chain are limited. They serve as a haven in times of predictable economic or political crises. Privacy coins can be sound money, and some of them have highly effective consensus mechanisms combined with industry breakthroughs in cryptography. But there are effectively no credit solutions built on top of these chains.

Unraveling the monetary history of mankind, we see that it is not only the concept of money that emerges but also credit and rehypothecation. The basic ideas of lending/borrowing money have led to the evolution of complex and intricate financial markets that we see today.

The rise of Ethereum introduced the concept of smart contracts. These 'Gen 2' chains enabled Dapps to be built on top of it. Thus kindling the fire for a swarm of new primitives such as DeFi, DAOs, NFTs, GameFi, etc.

In the world of crypto, DeFi meant that users could now obtain credit in a (somewhat) decentralized, trustless, and transparent manner. But as I alluded to earlier, the transparent nature of public blockchains has limited the number of applications that can be built on top of it. While there are tens of billions of dollars flowing through DeFi today, in order to bring in trillions of dollars worth of value, privacy is one of the key missing puzzles in all this.

Unfortunately, Ethereum faces the same drawback as other public blockchains. The state and all smart contract data are public by default. This severely handicaps the construction of financial applications where privacy as a feature is a requirement.

The bottom line is that in crypto, the privacy problem is a transparency problem. DLT technology was built to be transparent from its inception. While public blockchains prevent the likes of Web2 giants from monetizing our personal data, it opens the door for numerous other vehicles of informational asymmetry and socio-economic exploitation. In order to tackle this issue, there has been a handful of 'Gen 3' chains that emerged over the past 3–5 years. Giving birth to the beginning of PriFi (private finance).

A few of the PriFi projects that have made significant strides in this sphere are layer 1s that are chain agnostic ( interoperability is nearly as important as privacy). Not only do these chains allow for transactional privacy, but also enable programmable privacy. Thereby giving developers the freedom to choose the degree of transparency of smart contract data.

What is important to note here is that some of the leading projects in this space, despite the privacy element, do not prevent auditability. An individual - if they wished to do so - has the option to share her 'viewing key' with which a third party can audit her actions on the blockchain. This is important. As it gives the users a choice to remain private or not. Because of this elegant feature, I tend to disagree with that Ryan Gentry on this matter. To me, this is perfect privacy. It does not prevent auditability, but enables it.

So what does the ideal privacy-preserving blockchain look like?

From my perspective, for a certain application in PriFi to be successful (purely from a technical standpoint), it needs to be characterized by the following:

Decentralized - at least 10,000 nodes if PoW. Or a minimum of 2000 validator nodes if PoS. No compromises.

The native token must serve as a sound store of value — just as BTC does.

It has to be a layer 1 with programmable privacy.

Financial Dapps can be built on top of it.

It permits auditability at the user’s discretion.

To summarize the points above, the ideal privacy-centric chain must first and foremost be sufficiently decentralized. It is then imperative that the native token has real utility. And one such means of utility should be for it to act as a store of value. The chain needs to be a layer 1 in order to enable interoperability. Additionally, programmable privacy allows developers to build financial Dapps that offer credit solutions without compromising sensitive data. Finally, the cherry on top of the perfect privacy cake is to allow for auditability if and when required.

All of the information above is based on my own personal opinion. None of it should be considered or construed as professional financial advice. DYOR.

Recommend

About Joyk

Aggregate valuable and interesting links.

Joyk means Joy of geeK