The Evolving Landscape of Digital Payments: Why Blockchain Holds the Key

source link: https://hackernoon.com/the-evolving-landscape-of-digital-payments-why-blockchain-holds-the-key

Go to the source link to view the article. You can view the picture content, updated content and better typesetting reading experience. If the link is broken, please click the button below to view the snapshot at that time.

The Evolving Landscape of Digital Payments: Why Blockchain Holds the Key

Listen to this story

BAXE enables the world’s first truly open and connected digital economy.

“The convergence of smartphone, blockchain, cloud, AI, 5G and other technologies, together with the democratization of social access and increased deregulation (financial services) is enabling a paradigm shift in the creation of new payment products, platforms and services.”

- Andrew Broad, COO of BAXE

Cash may be king, but digital payments are coming for the throne! Whether you like it or not, the payments industry is undergoing radical change.

Whilst the payments industry was already on an upward trend on the digitization scale, the Covid-19 pandemic accelerated the process as demand by consumers for different forms of payment increased in order to minimise contact as much as possible in the midst of this global crisis.

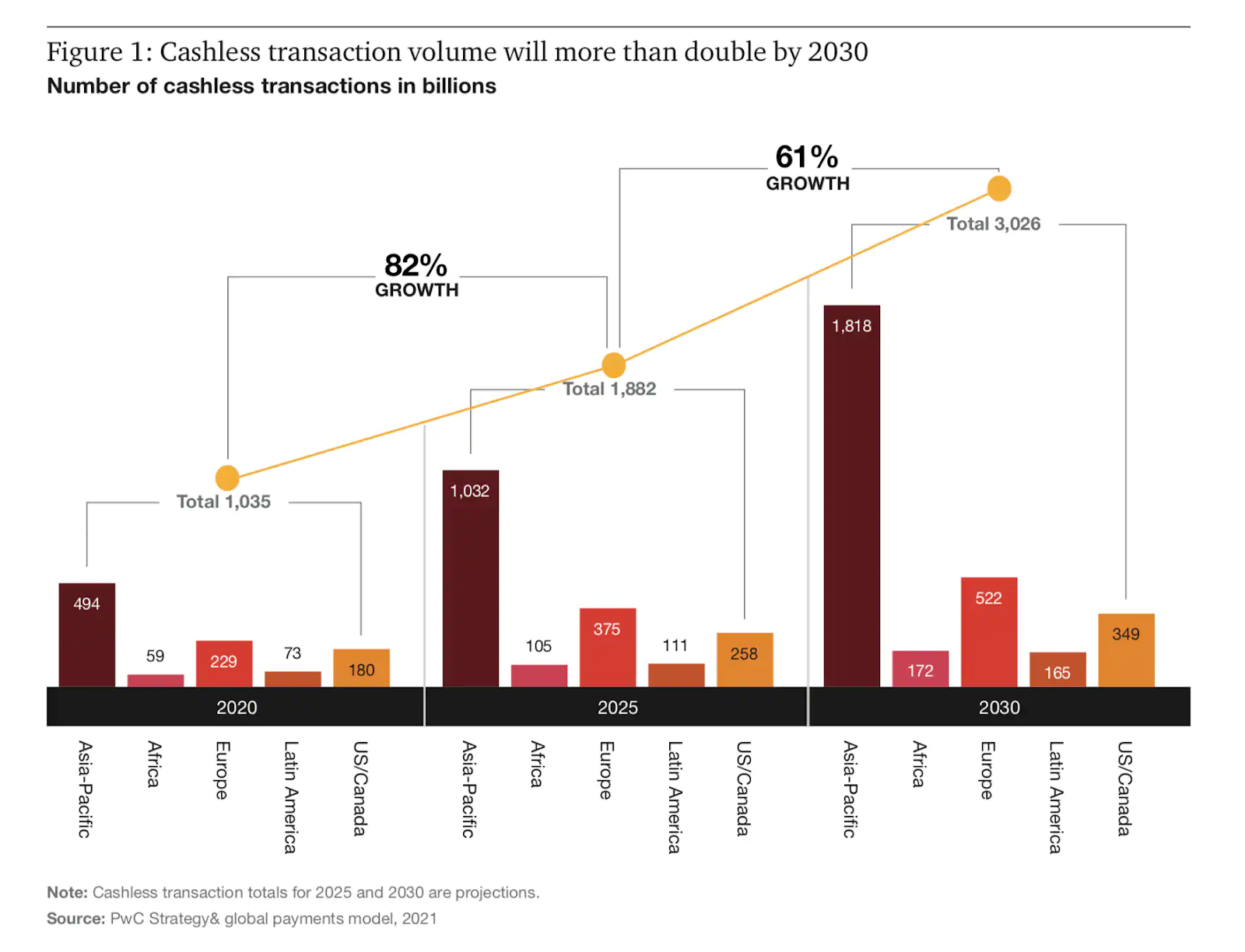

According to__reports__, digital payment volumes are set to grow by more than 80% from the year 2020 to 2025, from approximately 1 trillion transactions to nearly 1.9 trillion, almost tripling to about 3 trillion by 2030.

It is said that Asia-Pacific (APAC) will advance quickest with a projected volume increase of 109% by 2025, and an added 75% from 2025 to 2030.

When did the digital payments revolution begin?

Western Union pioneered the digital remittance movement when the company first debuted its electronic fund transfer (EFT), commonly known as “wiring” in 1871. This served as a quick solution to many who needed to send money near or far. In the early 1900s, the Federal Reserve started to transfer money via telegrams and wiring money became Western Union’s primary business.

Western Union did not stop there; the company further upped their game in the payments industry in 1914 when it introduced charge accounts. These accounts worked by linking to cards of customers who could then use it to purchase items on credit. The “charge card” was the start of credit in the industry, providing users with funds to make purchases but requiring balances to be completely paid off at a predetermined interval. It became quite commonly used throughout the first half of the century.

The industry further evolved with the introduction of credit cards in the 1950s. Fast forward to the internet era, electronic payments began to rapidly advance.

Web 2.0

The invention of Web 2.0 set the stage for not only the rapid advancement of electronic payment systems but also the introduction of merchants to participate in what we know today as e-commerce. Amazon, one of the pioneers of eCommerce and the go-to virtual store for most of us, was founded in 1994.

With e-commerce at the forefront of quicker and more efficient forms of cardless transactions, this led to the introduction of electronic verifications systems that allowed consumers to quickly verify and authorise digital payments from various channels. Not long after, mobile devices became popular methods of payment allowing consumers to pay for goods and services at the tap of a button through mobile wallets such as Apple Pay and Google Pay.

APAC continues to lead the digital payments revolution

E-commerce continues to grow with a projected growth of more than $4.6 trillion by 2022. The primary drive behind this is the lightning speed of which payments technology continues to evolve in the APAC region. Digital leaders such as Grab and Alipay continue to compete head to head in a battle to optimise their operations and provide the best possible customer experience. The adoption of various E-wallets such as GrabPay and WeChat has become increasingly popular in the region.

E-Wallets have proven to be able to integrate encryption, biometrics, tokenization and device authentication, setting the bar high and redefining the list of what’s possible in the digital space.

Blockchain-based global payments network

So, what holds the key to the future? Simply put, blockchain-based global payments network.

According to the World Economic Forum, by 2025, nearly 10% of global GDP will use either blockchain or blockchain related technology. Blockchain is a decentralised, digital ledger that facilitates the process of recording transactions as well as the tracking of assets in a network. It is a system that records information in a way that makes it nearly impossible to hack or cheat the system. Similarly, a blockchain-based global payments network is a decentralised system that facilitates payment messaging as well as clearing and settlement for all currency (i.e. fiat & digital) transactions in a single network.

Evidently, a blockchain-based global payments network will be significantly beneficial. Firstly, a blockchain-based global payments network is not restricted by geographic borders; it exists anywhere and everywhere as long as there is internet access. All you would require in order to access your data and manage your funds would be a private key. With this key, you would be able to perform any form of a transaction from anywhere in the world.

Furthermore, a major benefit of this payments network would be the ability to settle and clear transactions in one network. The beauty of a blockchain-based global payments network is the possible support of all types of currencies; both fiat and digital. This of course will serve as a simple solution to transactions anywhere in the world.

Blockchain-based global payment networks stay true to the saying, “time is money.” The time it would take to transfer money through a blockchain-based global payments network is similar to that of a cryptocurrency transaction; mere minutes.

Of course, one of the crucial benefits would be the transparency behind all transactions on the network. Through the use of a decentralised ledger that is multi-party validated, all transactions and exchange rates between currencies are immutable once agreed upon.

What’s to Come

With the evolution of technology comes the change in the global economy. Some firms may remain cautious and choose to opt-out of venturing within the blockchain space. Some may choose to take the leap and innovate within the space in order to revolutionise the industry.

So, what’s the next big game-changer in the industry?

BAXE is a pioneering integrated communications and peer-to-peer exchange platform, leveraging distributed ledger technology (DLT) and the innovation behind blockchain technology to create a super dApp that is set to usher in a new paradigm of integrated payment systems.

The BAXE dApp combines banking-level functionality with high-level, sophisticated communications channels. BAXE brings all these features into an easy-to-use space with an accessible interface.

With blockchain at the forefront of the digital payments revolution, it is bound to be a major influence in transforming the industry.

Recommend

About Joyk

Aggregate valuable and interesting links.

Joyk means Joy of geeK